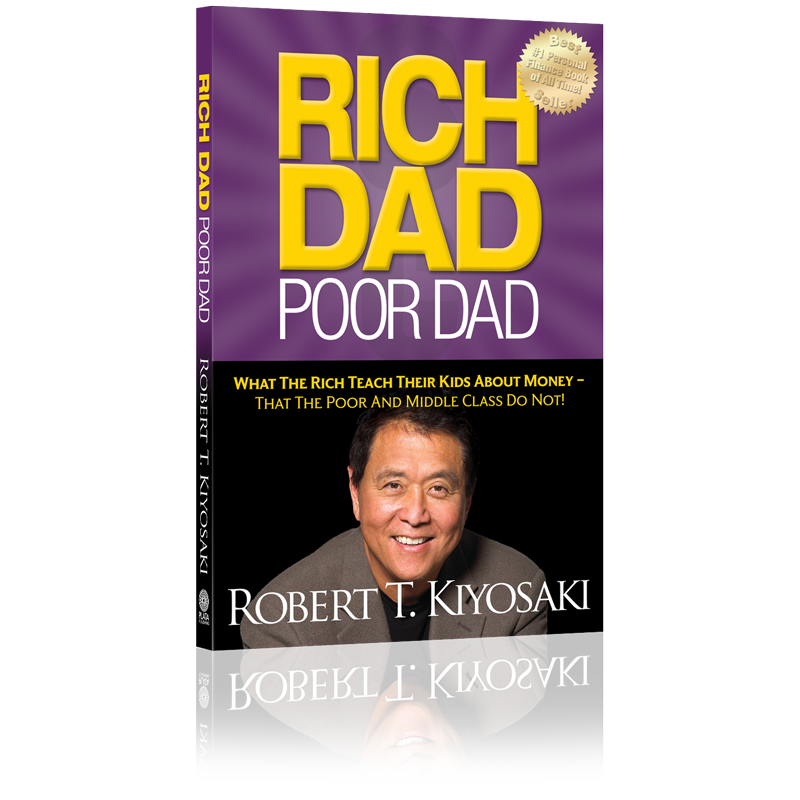

Rich Dad Poor Dad by Robert Kiyosaki with Sharon Lechter

If you have zero financial intelligence (‘the mental process via which we solve our financial problems’) do read this book. If your financial intelligence is top notch definitely read this book. And if you are just about able to manage your finances, ‘working for money’, living paycheck-to-paycheck or are starting out on your adult working life, this book is for you.

The short version of this review: The book Rich Dad Poor Dad is like a Nikon D3X camera. You can use it to make award winning photograpy featured in the National Geographic or you can use it to take memorable photographs and share on facebook and twitter or you may end up trashing the photographs you take but in the bargain will learn a thing or two about focus, angles and lighting.

The longer version. The book spoke to me at two levels. One at the essential level of information and empowerment regarding money and investments and two at the existential level of personal phobias and prejudices regarding money. While the former is definitely the central theme of the book, the latter is a recurring byproduct because when it comes to dealing with finances as with most things in life we are human and not robots.

Kiyosaki’s book gives you a tool an 11-year old will understand and he develops it to a level, giving advise on how to sieze real estate deals in a distressed market or at the foreclosure department of a bank that Donald Trump values. “You must know the difference between an asset and a liability, and buy assets. If you want to be rich, this is all you need to know. It is Rule No. 1. It is the only rule.” He goes on to say, “Rich people acquire assets. The poor and middle class acquire liabilities, but they think they are assets.”

His definition of asstes and liabilities is different from how a typical accountant would define them. He says in the book: An asset is something that puts money in my pocket. Period. A liability is something that takes money out of my pocket. Assets give you income. Liabilities add to your expenses. Stocks, bonds, mutual funds, real estate, intellectual property are all assets because they give you income in the form of dividends, interest, rental income and royalties. Mortgage, consumer loans, credit cards are liabilities.

He also says one of the toughest arguements he faces is when he tries to convince people that the house they live in is not an asset. The bigger and flashier the house you own and live in the greater the liability it becomes because it takes money out of your pocket towards mortgage payments etc.

One of the reasons the rich get richer according to Kiyosaki is that their assets generate enough income to cover expenses, leaving them with a balance to reinvest in more assets that continue to grow and the income it produces grows as well.

He presents a quadrant which is simple and will make you reflect. The right side of the quadrant reflects his Rich Dad’s philosophy towards gaining freedom by choosing to be a B (top right) or Big Business owner and I (bottom right) or Investor. The left side reflects his Poor Dad’s philosophy which his poor dad believed lead to security by choosing E (top left) or to be an Employee or S (bottom left) a Self-employed or Small Business owner. He does point out that with retirement schemes and stock plans Es can transition to the I quadrant.

In a chapter called The History of Taxes and the Power of Corporations, Kiyosaki explains how the rich diminish their taxable income. Knowledge of accounting, investment strategies, markets and the law are essential. Some of his advise in this regard may be considered risque in terms of accessing information and ways of minimizing taxes. But on reading the book one sees that he does buffer it with enough caveats for the discerning and the impressionable reader.

The middle class struggle according to Kiyosaki because their main source of income is their salaries which would increase but then so would the taxes they pay. He also says the middle class treat their home as their primary asset, instead of investing in income-producing assets.

There are people who give Kiyosaki a standing ovation at his lectures and say he has changed their life. There are others who say he is just a promoter of network marketing organizations. I first started reading this New York Times best selling book in 2002 and then in 2006. Third time in 2012 I started and completed. It may help to read repeatedly so it registers and to gain real value from this book let it give the impetus required to take action.